Tags

Brand, Case Study, Hershey, Hershey Company, HSY, International

One of the major precepts behind this blog is that we can learn the most about how profits are created by studying profitable companies and figuring out their business models. We can then think about how they might apply elsewhere. Hershey’s (HSY) is one such company.

In his 2011 letter to shareholders, Warren Buffett approvingly quoted the old business adage “buy commodities, sell brands.” “(This formula) has produced enormous and sustained profits for Coca-Cola since 1886 and Wrigley since 1891,” he added. “On a smaller scale, we have enjoyed good fortune with this approach at See’s Candy since we purchased it 40 years ago.” Why is this such a successful formula? If you can buy cheap commodities, imbue them with the special qualities we call a brand, and sell it at a high mark up, you have a winner. If you can turn your commodities into not just a brand but the very “currency of affection,” you have one of the all-time great companies. That is what Hershey was able to accomplish.

Hershey Stock Performance, 2001-Present

Background

Hershey is the largest producer of chocolate in North America and a global leader in chocolate and sugar confectionery. Its principal product groups include chocolate and sugar confectionery products; pantry items, such as baking ingredients, toppings and beverages; and gum and mint refreshment products. The company had sales of $6.6 billion in 2012 and sells in approximately 70 countries, although its business is centered in North America.

The Company has several iconic brands including Hershey’s Kisses, Jolly Rancher, Icebreakers, Reese’s and Hershey’s. The Hershey’s brand, about which we talk more below, is an American staple and has been passed down for generations. This scene from the television show “Mad Men” conveys the power of the brand much better than we can.

Industry Structure

We favor relatively slowly evolving industries that are duopolies or have three primary players. The US candy market certainly fits this description. We don’t anticipate any major new developments in confectionary technology and the industry is effectively a duopoly. Hershey and privately held Mars together control about 65% of the US candy market and it has been this way for many years. (Contrast this with the US weight management industry with hundreds if not thousands of participants and frequent new trends.)

The chocolate industry is characterized by high levels of brand loyalty. For whatever reason, chocolate brands are particularly powerful. As we saw with See’s and again with Hershey, consumers have an emotional connection with chocolate. It’s almost impossible to imagine a chocolate bar labeled simply “chocolate” gaining much traction. In fact, private-label competition is minimal in the confectionery market, at just 5% of the overall industry (versus the approximate 20% share private-label offerings maintain within the total food and beverage landscape). More on the below.

Eight of the top 10 chocolate brands in the US were introduced more than 50 years ago. The newest was introduced 20 years ago. All of the top brands are manufactured by either Hershey or Mars.

2012 US CMG Market Share (WSJ)

Mars 31%

Hershey 24%

Mondelez 6.2%

Nestle 3.3%

Lindt 2.3%

2012 US Chocolate Market Share

Hershey 43%

Mars 30%

Nestle 6%

Does Hershey Have A Moat?

Quantitative Evidence of a Moat

- High ROIC: Hershey has been able to maintain high returns on invested capital. (See Chart 2.)

Chart 2 (Click to expand)

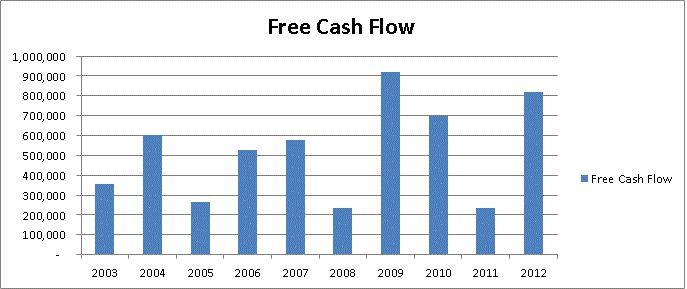

- Free Cash Flow: FCF has grown at a fast clip and is regularly greater than reported earnings. It dipped in 2011 do to a sharp increase in capex but otherwise has been very reliable. See Chart 1.

Chart 1 – Hershey FCF, 2003-2012 (Click to expand)

- Stability of Market Share: One of the hallmarks of a great business is very little competition. As discussed above, Hershey and Mars have controlled the US market for decades.

- Here is how Hershey compares to our standard, Moody’s (MCO):

| Hershey | Moody’s | |

| HSY | MCO | |

| Market Cap as of 7/16/13 | 20.58 | 13.42 |

| Net Debt | 802,695 | (166) |

| Revs | 6,644 | 2,730 |

| OI | 1,111 | 1,090 |

| Op Margin | 17% | 40% |

| NI | 661 | 700 |

| Net Margin | 10% | 26% |

| ROA | 14% | 20% |

| ROE | 63% | 647% |

| ROIC | 48% | 61% |

| Klarman Factors | ||

| Barriers to Entry | High* | Very High |

| Capex/CFOA -10 year avg, | 34% | 7% |

| Reliable Customers | Very High* | Very High |

| FCF/Revenue – 10 year avg. | 12% | 28% |

| 5 Year FCF CAGR | 36% | 17% |

| 10 Year FCF CAGR | 10% | 10% |

| *Limited to North America Market | ||

Qualitative Evidence of a Moat

Hershey has customer captivity in the form of brand loyalty complemented by economies of scale.

Brand Loyalty

A popular, well-known brand like Hershey is not necessarily a profitable brand. A brand alone does not create a moat. Instead, the brand must generate brand loyalty. Prof. Greenwald and his co-authors in both Competition Demystified and The Curse of the Mogul carefully distinguish between a mere brand and brand loyalty. His favorite example, cited in both books, is Mercedes Benz. Mercedes has spent millions building an image of luxury and power yet has never generated above average returns. By contrast, other companies have hit upon the special alchemy that creates brand loyalty. We tend to use the terms “brand” and “brand loyalty” interchangeable but the distinction is illuminating.

Brand loyalty generates above average returns through two avenues: pricing power and repeat business. If a company can charge more for its product or if consumers habitually buy its product, the company certainly has a competitive advantage. One of the most dramatic examples of the power of a brand is Bayer aspirin. Why does anyone buy Bayer aspirin — or Tylenol, or Advil — when, almost always, there’s a bottle of cheaper generic pills, with the same active ingredient, sitting right next to the brand-name pills? Bayer can charge twice as much as a generic competitor.

Coca-Cola , by contrast, has brand loyalty in the form of habit but it does not have pure pricing power. Coke can charge more than generic colas but it cannot charge more than Pepsi. As a result, Coke is not getting significant returns on its brand advertising.

Hershey is in a very similar position to Coke. It has a well-known brand name which resonates with a segment of the population who buys its products religiously. But it is not able to charge more than Mars. This is not to say that the Hershey brand is not valuable. Its simply to state that on the spectrum of valuable brands it is less valuable than Bayer or See’s.

Economies of Scale

While not a classic high fixed cost business, due to relatively high input costs, Hershey does have economies of scale in the following areas:

- Manufacturing – Hershey’s huge scale allows it to practice mass production techniques that reduce the cost of production per unit

- Marketing – We cannot forget that Hershey’s brand recognition is largely due to enormous expenditures on advertising. Hershey has dramatically increased its investment in its brands to widen the moat. Advertising expense represented just 2% of revenues in 2006 but jumped to 7% in 2012. Management has pledged to continue to increase advertising expenditures. Due to economies of scale in advertising, HSY can afford to spend much more than any of its competitors other than Mars.

- Distribution – Hershey’s high density of customers in North America allows it to build economies of scale in distribution. Hershey serves the North American market out of 4 distribution centers. Each center serves many customers, reducing the amount of distribution expense per customer.

- Research and Development – Hershey is able to spread R&D expense over many more units than any smaller competitors.

The US candy market evolved into a duopoly because both Mars and Hershey developed economies of scale for the national market. When economies of scale are combined with customer captivity in the form of brand loyalty, it is a powerful combination.

As the leading brands, Mars and Hershey can charge a premium for their products. A competitor is free to try and undercut them on price. But if Mars and Hershey are vigilant, they will simply cut their prices below the price where their competitor who has no economies of scale. This is known as the entry deterring price. Because Mars and Hershey can spread their fixed costs over so many units, they can charge a low enough price to deter new entrants but still command large profit margins.

Economies of scale are so important in this industry that, over the years, competition has been reduced to just two players, Mars and Hershey.

Together, Hershey’s brand loyalty and economies of scale create prodigious obstacles for any new entrant to the North American chocolate industry to overcome. First, a new entrant would have to spend a fortune replicating the fixed costs associated with the business, including distribution, marketing and sales, manufacturing and R&D. Having replicated the high fixed costs of Hershey, a new entrant will then have to recruit new customers to support that infrastructure in an economic way. Because of Hershey’s brand loyalty, a new entrant will have to offer a higher quality (more expensive) product or undercut Hershey on price. But Hershey, with the benefit of lower average cost, can always match or even outdo any introductory offers of this sort. To the extent there are any unattached customers, Hershey can sell at a much lower price than the new entrant because of this lower average cost.

All of this sounds highly theoretical, but we do have two real world examples. Both Nestle and Cadbury are highly capitalized, multinationals with deep pockets and patient owners. After years and years of effort, neither has made much of a dent in the Hershey/Mars duopoly in North America.

Pricing Power

One of the clearest indications of a moat is the ability to raise prices without fear. As discussed earlier, Hershey has limited pricing power. Hershey can raise prices but only in concert with Mars.

As we saw in the Hertz discussion, the more concentrated the market, the more the natural competitive pressure to lower prices is blunted. The US candy duopoly of Mars and Hershey reflects this and has been remarkably cooperative. Just over the past 4 years, the company has raised prices 10% in 2009, 2.4% in 2010, 3.5% in 2011 and 5.7% in 2012.

The candy duopoly has been spared any costly price wars. A 1999 article by James Surowiecki explained this dynamic: “Say Mars wants to cut prices on its Bounty bars in order to take customers from the market-leading Mounds bar, produced by Hershey. What happens next? Hershey will probably cut prices to match. But the market-leading product often costs less to make than the others—you can do greater production runs and spread fixed costs like advertising and design across a larger number of sales. Without any backroom meeting, Hershey sends a very clear signal: cutting prices will cost Mars money, with no market-share gain. The next step in this dance is usually a restoration of prices to the old status quo.”

Management and Capital Allocation

Hershey has a refreshingly stodgy reputation for capital allocation. Hershey Trust Company, as trustee for the benefit of Milton Hershey School (frequently referred to as the “Milton Hershey School Trust” or the “Trust”), maintains voting control over The Hershey Company. The Trust is seen as valuing steady and consistent cash flows over risky growth investments. Consistent with this, the Company has returned an average of 146% of FCF to shareholders in the form of share buybacks and dividends over the period 2003 to 2009. Management has stated that their goal is distribute 50% of earnings to shareholders. Given the Company’s wide moat in the slow growth US market and limited growth opportunities elsewhere, this approach makes perfect sense. (See Chart 3.)

Chart 3 (Click to expand)

However, Company communications seem to be developing a new emphasis on revenue growth with no corresponding focus on FCF or even EPS. The Company went so far as to create a new position, Chief Growth Officer. Quotes like this from the new CGO give us pause: “We want to be at $10 billion in revenue in the next five years, which calls for a very aggressive top-line growth rate. We want to transform the geographic footprint to have 25% of our revenue coming from international, and we want to expand our portfolio, leveraging [mergers and acquisitions] and innovation.” (Michele Buck, SVP and Chief Growth Officer, Forbes, 3/4/13). Why focus so much on topline growth? Why no mention of earnings or cash flows? Why set arbitrary goals like $10 billion of revenue or 25% for international revenue?

Further at a recent investor conference, the Company trumpeted its “big bet on China” and its revenue growth there and in other emerging markets. Again, no mention of profits. They even resort to non-GAAP measurements like “adjusted gross margin” which is never really defined but seems to be gross margin with certain “non-recurring” items that show up in Cost of Sales added back.

A review of press coverage of Hershey’s international expansion shows no one questioning the basic premise. Instead, the complaint seen over and over again is, why is it taking so long?

With these thoughts in mind, let’s take a closer look at Hershey’s international expansion.

New Territory Brings Risk for Hershey

Returning to our basic framework, a company is only attractive to us if they have a wide moat that protects them from competition and keeps ROIC from reverting to the mean. Investments outside the moat are value-destroying and should be avoided. Nevertheless, many companies feel pressure to grow revenue and cannot resist the temptation to invest outside the moat in the hunt for revenue growth. A company that simply wants to grow, without consideration for its moat, will perhaps be able to increase its size, but will see its profitability go down inexorably.

Neither of the two main components of Hershey’s moat, brand loyalty and economies of scale, are present when Hershey ventures overseas.

No Brand Loyalty

New customers, unlike existing ones, have no brand loyalty. New entrants in a market have a level playing field when competing with incumbents for customers in virgin territory.

What competitive advantages does HSY have in emerging markets where the Hershey brand is entirely unknown and where local tastes are dramatically different than the US? Far from being the “currency of affection,” Hershey is trying to introduce the population to the very idea of a chocolate bar. Because tastes and preferences for snack offerings vary around the world, Hershey will need to invest to ensure that it understands the local consumer, rather than just launching products that have worked in its home market.

This is particularly true with chocolate. Nestle has been unable to compete with Hershey in the US or Cadbury in the UK. See’s limited expansion outside its core territory of the Western United States is instructive. See’s spends the lion share of its marketing budget on widening its moat in this territory and engages in very limited expansion in the rest of the country.

No scale advantages

The other key component of the HSY moat, economies of scale, is also not present overseas.

Quite simply, until and unless Hershey hits critical mass in China or any of the overseas markets, none of the economies of scale outline above will be present. For instance, the expenses associated with an R&D center Hershey recently opened in China will be spread over many less units than its North American counterpart or its larger competitors in China. Beyond R&D, adapting the product and packaging for local tastes will create added costs in production.

Despite these obstacles, Hershey continues to invest overseas. China, in particular, has an allure that Hershey can’t resist. Hershey has been trying to crack the Chinese market since the 1990s with no luck. It is way behind its competitors with just a 2.2% market share in 2012. Chocolate is still a relatively new category to many Chinese consumers, with all the attendant educational challenges. Recently, in apparent recognition of this uphill climb, Hershey launched a new milk candy product solely for the Chinese market. It is Hershey’s first new product launch outside of the US. This move seems like a bit of a head scratcher to us. What could be more expensive and risk y than a new product launch? Does Hershey have any kind of a moat in the crowded Chinese milk candy market?

We are not sure what unique qualities HSY brings to the table in China, Brazil or other countries. Making a frontal assault on its more established competitors seems doomed and expensive. HSY would be better off doing what its big competitors are not doing.

Unfortunately, Hershey management seems to be unaware of the nature of its moat. By remaining a regional player in the North American market, Hershey heightened its scale advantages and capitalized on its brand loyalty. By expanding outside its core region and into foreign markets where it has no scale advantages or loyal customers, Hershey operates with no moat and is unlikely to earn more than its cost of capital. As we would expect, this issue is reflected in the income statement. Over the past 10 years, Hershey’s SG&A expense grew at a CAGR of 9%, nearly twice as fast as revenues.

Luckily, Hershey’s international expansion has been fairly focused and disciplined to date. The CEO continues to say all the right things and maintains that international investment will not put the key US market in jeopardy. “We want each of these markets to be successful for us,” he said on the Q1 2013 earnings call. “We want them to be rewarding for our shareholders and therefore we have a pretty planned approach and we don’t want to get out of balance with what is a very precious North American business and so our approach, I think, frankly is very advantaged and at the same time, maybe not the same choice that everybody would have, because they may have legacy businesses that don’t allow them to look at this in the same way that we do.” Nevertheless, he too is touting arbitrary revenue goals.

ROIC and ROE continue to remain high as well. ROIC in 2012 was 48%, 2 points ahead of its historical average of 46%. ROE was 63%, 4 points ahead of the historical average of 59%. Further, the commitment to the dividend acts as a nice limitation on any foolish overseas expansion. Total capital investment (capex + R&D + M&A + advertising) is starting to creep up though. In 2012, it was 7% of revenue, 2 points ahead of its historical average of 5%. If the overseas expansion is not profitable, this level of investment will eventually cause ROIC to drop.

Conclusion

In a nutshell, Hershey drives high return on capital and is a revered American brand. The result is prodigious free cash flow that is available to be returned to the owners as dividends or share buyback. It sells a discretionary product but one that consumers cherish and is priced modestly. Finally, none of this is likely to change as it is sheltered from competition by being in a naturally occurring duopoly with stable market shares. No new entrants no new entrants are likely to breach its moat. The one cloud on the horizon is the push for expensive overseas expansion that is unlikely to succeed.

If we return to the characteristics of a good business that Seth Klarman listed, Hershey hits nearly all of them:

- Strong barriers to entry Check

- Limited capital requirements Medium

- Reliable customers Check

- Low risk of technological obsolescence Check

- Abundant growth possibilities Medium

- Significant and growing free cash flow Check

As stated previously, almost all businesses we look at will be inferior to See’s and Moody’s. Most noticeably, Hershey requires far more capital investment than See’s or Moody’s.

So how do we value Hershey’s? Acknowledging that valuation is more art than science, let us proceed. Enterprise value, as you know, is defined as stock market capitalization plus debt less cash, although there are many twists on this basic formula.

Let’s start with 227 million fully diluted shares. There are 60 million B shares held by the Trust that do not trade and have enhanced voting rights and reduced dividend rights, but we will assume for these purposes that they have the same value as the publically traded common shares. This gives us a market cap of $20.9 billion, using the August 30 closing price of $91.95. We then add $1.9 billion of debt, $250 million of unfunded pension obligations, and $318 million of other post-employment benefits (OPEB). This adds up to $23.37 billion.

We then subtract $728 million of cash and cash equivalents.

This gives us an enterprise value of $22.64 billion. We assume that Hershey can produce $884 million of EBIT. This is an average of the past 5 years and is very conservative as EBIT has increased by !5% CAGR over the past 10 years. Dividing $884 million by $22.64 billion, we get an EBIT yield of just 3.9% (or an EBIT multiple of 25.61). This is a bit pricey for us. Hershey as a tightly focused company with leading brands and high growth rates is currently in Mr. Market’s good graces. Nevertheless, we will add Hershey, a venerable American brand, to our watch list.

UPDATE: I stumbled across this article earlier today. I found it funny and interesting as well as relevant.