Jamie Dimon, the chief executive of JPMorgan Chase, warned in his 2014 annual shareholder letter in 2015 that “Silicon Valley is coming” for banking’s bread and butter. It was a pivotal moment, because traditional banks are deep-pocketed monsters with large branch networks, huge marketing budgets and many years of underwriting experience. Could one of these Silicon Valley companies, OnDeck (ONDK) really take on these behemoths? To put the size difference in perspective, Chase spent $2.5 billion on marketing in 2014. ONDK had $73 million of net revenue. Chase extended $1.7 billion in business banking loans in the third quarter. ONDK has originated $3 billion loans in its lifetime. Was Dimon really concerned that they could cross the moat of regulation, longstanding customer relationships, marketing muscle, implicit government guarantee and deep pockets?

Just a year later, Dimon was forced to raise the white flag over Castle JPM and surrender to the forces of FinTech. On December 1, 2015, On Deck Capital, Inc. (ONDK) confirmed that it is working with JPM on a strategic partnership. JPM will use the Company’s small business lending platform to originate, underwrite and service loans to small businesses. ONDK will get fees to originate and service loans for Chase, many with a value up to $250,000, previously considered too small to move the needle at the big bank. OnDeck also can use data it gleans from the partnership to improve its data models.

While I typically prefer tried and true businesses to glamorous and fast-growing Internet companies, I found this company and its model interesting enough to do a deeper dive. In particular, I am impressed by ONDK’s ability to benefit from network effects.

What Does ONDK Do?

ONDK is an online lending portal for small businesses.

ONDK has four models for originating loans.

- Originate & Retain – ONDK has large warehouse facilities at reasonable rates. These funds allow ONDK to originate and retain most of the loans originated. ONDK has first loss position on all bank facilities

- Originate & Securitize – ONDK also securitizes their loans. ONDK retains a 5% first loss risk position on all securitizations.

- Originate & Sell – 35-40% of loans are sold at a premium to institutional investors via the OnDeck Marketplace.

- Software as a Service – In the arrangement with JPM, ONDK will be acting as a software as a service provider. It will originate and service loans but it will provide no funds and it will take no credit risk.

ONDK’s median business customer has been in business 7 years, has a physical location and has $600,000 in annual revenue.[1]

The three most common uses of OnDeck credit are the purchase of inventory, employee hiring and retention, and the acquisition of new business equipment.[2] The loans fall somewhere between a long-term loan from a traditional bank and credit card debt.

Nearly all the debt held on ONDK’s balance sheet is non-recourse. Many of these loans operate similarly to a merchant cash advance, with a fixed amount or percent of sales deducted daily from the borrower’s bank account over several months. Given the short loan terms, the rate a small business borrower could pay on an annualized basis is a median of about 50 percent at ONDK for a business term loan, but can range anywhere from 30 percent to 120 percent, with average loans of about $40,000.

ONDK gets customers through three channels: direct marketing, strategic partners (banks, technology companies and companies serving small businesses) and brokers. ONDK is de-emphasizing the broker channel after getting in bed with some unsavory characters. (See Chart 1).

Chart 1

Source: 10-Ks via sentieo.com

Total Addressable Market

The total addressable market seems sizable. There are estimated to be $800 billion of small business loans in the US. ONDK targets loans under $250,000. According to the FDIC, there were $186 billion of loans in this segment in Q2 2015. In any case, with just $1.7 billion of originations in the last 12 months, ONDK would seem to have a long runway ahead of it.

Competitive Landscape

The competitive landscape has been stable for decades but is in a state of flux. The traditional banks dominate the market but are not serving it well.

The primary problem is that unit economics do not allow them to offer the small, short term loans that small businesses need. The cost structure of traditional bank – which include an extensive branch network, in person meetings, a costly staff of loan officers – is supported by the relatively large size of the loans they offer. The unit economics break down at smaller loan amounts. For the traditional banks, the cost of processing a $100,000 loan is the same as processing a $1,000,000 loan. As a result, small business loans are generally not worth the trouble.

Second, traditional banks have not developed an underwriting process tailored to small businesses. Wide heterogeneity, high failure rates, and varying use of borrowed funds make it hard to develop general standards. There is no widely-accepted credit score for small businesses. Rather than devoting resources to solving this problem, traditional lenders simply rely upon the small business owner’s FICO score as a primary indicator of the business’s creditworthiness, even though it is not necessarily indicative of the business’s credit profile. As a result, traditional banks use a long, time-consuming loan application process that takes on average 33 hours to complete.[3] This is a non-starter for time and resource constrained small business owners.

Small businesses whose needs are not being met by traditional bank loans resort to a fragmented landscape of products, including merchant cash advances, credit cards, receivables factoring, equipment leases and home equity lines, each of which comes with its own challenges and limitations.

Alternative online lenders, including ONDK< have rushed to fill this niche. The online loan market is very small but growing fast.

Online lenders fall into seven broad categories (see Chart 2) :

- Traditional balance sheet lenders: These firms lend out their own and retain the loans on their balance sheet.

- Marketplaces: Marketplace lenders provide a platform where lenders and borrowers can meet. The marketplaces add value through the matchmaking process, credit risk assessment, pricing and loan servicing

- Crowdsourced Platforms: Crowdsourced platforms facilitate equity funding

- Aggregators: Aggregators allow borrowers to comparison shop a range of loan products which are offered from a variety of sources. The value added is the reduction of search costs.

- B2B Invoicers: These firms help small businesses with the invoicing process. This puts them in a position to understand these businesses cash flow patterns and suitability for short-term loans. Because of this access to data, many are now adding lending to their bundle of services.

- Payment Networks & E-Commerce Platforms – These companies also enjoy privileged access to data making the underwriting process much easier. As a result, these companies are also offering short-term financing to their customers.

As described above, ONDK is a bit of a hybrid, falling into both category #1 and #2.

Chart 2

Source: Oliver Wyman & QED Investors, “The Brave 100: The Battle for Supremacy in Small Business Lending”

The Online Lenders’ Strategy

“Disruption” is an overused word, but it certainly seems to apply here. The online lenders have a four-pronged strategy in their asymmetric battle against the traditional banks.

The first prong is a data-driven approach to underwriting. The online lenders reject use of the FICO score. Instead, the online lenders tailor their underwriting approach to this market segment. They take into account information from a wide range of sources including data on online banking, accounting, bookkeeping, credit card, shipping, supplier, and social media. For example, ONDK’s automated model pulls from more than 100 external data sources, and analyzes more than 2,000 data points per application. This approach has greatly expanded small business access to credit.

ONDK claims their model eliminates is 90% accurate at a 40% acceptance rate while pure FICO can only achieve 40% accuracy with a 20% acceptance rate. In other words, they can enter into twice the number of loans as a FICO based system with the same level of risk.

Improved User Experience

As we have come to expect from Silicon Valley innovators, the online lenders have developed user friendly sites and apps. The online lenders focus on creating clean, simple and friction-free application processes. Much of the data collection process is automated. An application can be submitted in minutes and an approval decision and money transfer can happen the same day.

Lower Cost Structure

These online lenders can target smaller loans in an economically favorable way, enabling them to serve a generally under-banked segment of the market. Unlike the traditional banks, the unit economics allow online lenders to profitably make small, short duration loans. They also offer automated daily and weekly collection services.

Regulatory Advantage

These lenders are not currently directly regulated by the FDIC or the CFPB, allowing greater flexibility in offering different rates to different types of borrowers, thereby creating additional efficiencies.

What Makes ONDK Stick Out from the Crowd? Sources of Competitive Advantage

Data Network Effects

First and foremost, ONDK benefits from a particular type of network effects, data network effects. As I have written about previously, a network effect occurs when the value of a product or service goes up with the number of people using it. The classic example of network effects is the telephone. As more people bought telephones, the greater the likelihood you could reach someone which made the product increasingly valuable.

A less well understood type of network effects is data network effects. Matt Turk, a venture capitalist, recently described the concept of data network effects on his blog:

Data network effects occur when your product, generally powered by machine learning, becomes smarter as it gets more data from your users. In other words: the more users use your product, the more data they contribute; the more data they contribute, the smarter your product becomes (which can mean anything from core performance improvements to predictions, recommendations, personalization, etc. ); the smarter your product is, the better it serves your users and the more likely they are to come back often and contribute more data – and so on and so forth. Over time, your business becomes deeply and increasingly entrenched, as nobody can serve users as well.[4] (Emphasis in original)

In essence, a feedback loop is created that is difficult to disrupt. This feedback loop leads to the winner takes all outcome we see so often industries based on algorithms. This is how Google came to dominate Internet search. “The more people searched, the more data they gave Google to make its index better, smarter, faster, and, eventually, more personal. In short: as Google got bigger, it got better, which made it bigger still. Google is a winner that has taken it all.”

Chart 3, The Data Network Effects Feedback Loop

ONDK’s core business benefits from data network effects in several different and mutually reinforcing ways.

First, ONDK’s underwriting process is a classic example of data network effects at work: the more small businesses use the platform, the more data points they provide, enabling ONDK to refine and improve its ability to assess credit risk. This phenomenon creates a powerful competitive advantage. ONDK’sc credit models get better the more it lends and if it is lending more than their competitors in a given year, they should be getting better faster. There are “major benefits to the credit model at scale in terms of the data you have collected, the amount of lending outcomes you have observed. so you can take more intelligently informed risks, maybe, than a smaller computing platform could.”[5]

A new entrant to the industry is far behind ONDK. “And the thing about lending is you can’t go from zero to 60 overnight. You have to lend and learn. It’s an iterative process. And what we know is that there is substantial advantages that go to the scaled player. So if OnDeck is the leading originations volume player in the space, that means we’re going to learn more from that set of originations this year than a competitor who was lending at 1/10 the volume. We are probably collecting 10 times the data.”

Further the improved risk assessment via the OnDeck Score as well as the short term loans allows ONDK to expand access to credit. ONDK is able to help borrowers that the traditional banks or even some online lenders would reject out of hand.

Additionally, the superior underwriting process allows ONDK to streamline and automate loan applications, expedite underwriting and quickly price risk, and provide loan applicants with quick loan decisions and access to funds. Estimates show that applications at these creditors take as little as 1/50th the time to complete of those at traditional banks.[6] Reports suggest that some borrowers are willing to pay a higher price in exchange for an easy application process, a quick decision, and rapid availability of funds.[7] All of this is summed up by ONDK’s net promoter score of 75.

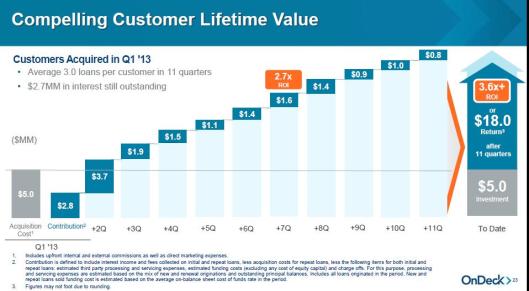

Similarly, as ONDK collects more data on its customers, its customer acquisition cost declines. A key scale benefit for ONDK is reduced customer acquisition cost. ONDK mainly uses direct response marketing, a highly measurable form of advertising. As they gain more experience, the marketing becomes more highly targeted and, therefore, more cost effective – increasing the gap between ONDK and its competitors.

Additional Scale Advantages

As most of my readers know, economies of scale exist when the unit cost of a product goes down as the volume of production goes up. Therefore, it is cheaper to make cars in factories that produce 300,000 cars per year than make them in factories that produce 2,000, and this is true even if the cars are basically identical.

A technology company like ONDK is highly scalable. Once the IT is in place and algorithm created, the marginal cost of processing a new borrower is extremely low. Accordingly, operating expense as a percentage of loans dropped from 12% in 2012 to 3% over the last 12 months.

ONDK’s scale also results in a reduced cost of capital. Breslow described the dynamic at an investor conference: “ When you look at cost of capital, that is also a game of scale, and bigger institutional lenders can offer you lower rates, but they are not going to do that unless there is enough capital to put to work on a scaled-up platform.” This leads to lower rates on borrower side.

Switching Costs

As discussed above, ONDK grabs the small business customer early in the business lifecycle when traditional banks and other lenders have the most trouble assessing the credit risk and when the dollar amounts are small. “So I think our opportunity really is we think we can underwrite a small business earlier in its lifecycle than any traditional bank can. So if you are two, three years in business, you’re just starting out, OnDeck should be able to work with you before a lot of our competitors can because we understand that incremental risk and we can underwrite that risk better than others.”[8]

Then, once they are in the door and the customer acquisition cost has already been incurred, ONDK strategy is to provide them with more loans. How? ONDK creates switching costs through its loyalty program. Under the loyalty program, for repeat customers origination fees are generally reduced or waived and interest rates are lower.

The lifetime value of these repeat customers is very high. The incremental costs of each additional loan are quite low as the customer acquisition cost is dramatically reduced on each successive loan. (See Chart 4.)

Chart 4

Brand

ONDK has become the go-to partner for banks looking to better serve this market. (See Chart 5.)

Chart 5

Source: Forms 10-K via Sentieo.com

How Will This Play Out Over the Next 10 Years?

Over the trailing 12 months, ONDK earned $4 million of operating income. To hit my hurdle rate of 15% per year, ONDK will have to earn operating income of $140 million in 2025. Using fairly conservative assumptions, I can get ONDK to hit this goal. My assumptions:

The most difficult assumption is the growth rate of originations. Yet, even at a 15% CAGR, the total loans projected to be originated in 2025 are just $7 billion. This is a small fraction of the total small business lending market, even assuming no growth in access to credit. As stated earlier, the total market for small business loans under $250,000, ONDK’s targeted segment, is estimated to be $186 billion.

What other outcomes are plausible? What could disrupt this projection? What is the likelihood that they occur?

Scenario #1 – The Traditional Banks Launch a Successful Counter-Offensive

In scenario #1, the traditional banks successfully beat back competition from ONDK. This seems highly unlikely.

Faced with competition from online lenders, traditional banks options are left with three options: (1) continue the status quo of simply ignoring small value loans, (2) build their own platforms, underwriting models, etc to handle small loans, or (3) partner with someone like OnDeck.

The traditional banks are fat, dumb and happy. They largely rely on the simple fact that every small business in the country has a checking account. This gives them a natural entrée to any company considering a loan. When combined with their marketing muscle, their branch network and share of mind, they have little incentive to change their way of doing business.

It will be easier to partner with OnDeck. OnDeck has built a machine. There is no sense in trying to re-create what OnDeck has done. Even if a bank tried to recreate OnDeck, they would struggle to get the data that OnDeck has – since OnDeck has many partners. Even if they had the data, there is an a question of how to underwrite using that data – which is nontrivial.

The JPM partnership deal indicates that the financial services industry has accepted the new reality and is adjusting accordingly. They realize that it is a fight that is unwinnable.

Scenario #2 – Competition from Other Online Lenders

In scenario #2, competitors are drawn to the market by ONDK’s high return. Increased competition reduces returns on capital for all participants to the cost of capital. I see this as somewhat likely.

Despite the competitive advantages described above, ONDK still has its vulnerabilities. There will likely be other winners. Some firms occupy a fortuitous position whereby their main business gives them privileged access to data on a firm’s cash flow and an advantage in pricing risk. American Express Merchant Financing has been successful for Amex, extending short-term financing to businesses that accept American Express cards and that have significant Amex-specific charge volumes. Similarly, Square has terrific data on their customers, and will be in the best position to offer their customers small dollar financing for inventory, etc. Same for Amazon. OnDeck can’t compete for those customers. As a result, ONDK needs to target a niche within a niche. OnDeck’s sweet spot is small business with a physical presence – plumber, landscaper, restaurant, etc.

Nevertheless, there is also some chance the market could tip to a winner takes all scenario. As discussed above, many Silicon Valley companies have emerged as monopolists due to network data effects and other scale advantages.[9] As companies get bigger, they get better, which makes it better still. Once a company emerges as the leader in a market, it is difficult to slow their momentum.

I think the likelihood of a tipping point is low due to the presence of these competitors with privileged access to data. But, the probability is somewhere north of zero and the reward is huge.

Scenario #3 – Self-Inflicted Wounds

Perhaps the great risk comes not from competition but from self-inflicted wounds. Nothing is more commodity-like than a loan. As competition proliferates, what will stop borrowers from simply shopping for the lowest rate and the loosest underwriting? ONDK’s interest rates are quite high, averaging ~40%. These rates provide plenty of room for competition to undercut them.

How will ONDK respond? Will they water down underwriting standards in order to maintain topline growth?

A commitment to maintaining high underwriting standards has proved difficult for financial services time and time again. Because one loan is indistinguishable from another, one common way to gain market share is to simply reduce underwriting standards. A deadly combination emerges: risk tolerance increases as interest rates go down. This dynamic has brought down many companies. The only solution if risk tolerance is high in the marketplace is to walk away from potential business.

But, while simple on paper, it is very difficult for companies to knowingly turn down business and contract rather than grow. Warren Buffett has written about this risk many times in the auto insurance (GEICO) context. Buffett refers to the impulse to grow even if it means increasing risk as the “institutional imperative.” “Most American businesses harbor an ‘institutional imperative’ that rejects extended decreases in volume,” Buffett writes. “What CEO wants to report to his shareholders that not only did business contract this year but that it will continue to drop?.”[10]

While every lending business would like to believe it makes loans only after applying strict underwriting criteria, it is hard to avoid the siren song of growth, especially for publicly traded carriers that have to worry about Wall Street.

The institutional imperative has such a strong pull that restraints must be put in place to avoid reckless loans.

One corrective is to incentivize employees to maintain underwriting discipline. For example, employees can be assured that no layoffs will take place if risk tolerance in the market increases and the company finds it best to walk away from new business. Otherwise, employees will rationalize inadequate pricing, telling themselves the poorly-priced business must be tolerated in order to avoid layoffs. Accordingly, Berkshire does not engage in layoffs when there is a cyclical downturn at one of the insurance companies. Buffett explained: “This no-layoff practice is in our self-interest. Employees who fears that large layoffs will accompany sizable reductions in premium volume will understandably produce scads of business through thick and thin (mostly thin).”[11]

As is typical of most companies, ONDK provides no information on their layoff policy. The business is not labor intensive. I would like to think they would prefer excess overhead to sloppy underwriting. Nevertheless, the financial metrics that executives are measured on are disappointing. Per the most recent proxy they include: overall financial performance, total units, new units and new products, development of OnDeck Marketplace and certain customer-related measures. Unfortunately, these are largely measurements of growth with no view as to whether the growth is profitable or risky.

ONDK argues, however, that the short term nature of their loans means that a deterioration in quality will show up quickly and be corrected. “So when you look at our business, you do see shorter terms than traditional bank loans, you do see more frequent collections methods than traditional bank loans. And we think that creates valuable early warnings and protection for us if economic circumstances were to change.”[12]

Another restraint on the institutional imperative is so-called “skin in the game.” That is, how much of the companies own capital is at risk? The originate-to-sell model came under a great deal of criticism in the wake of the financial crisis. The argument against this model was that loan originators cared little about the quality of loans because they knew the risk would land on someone else’s balance sheet. Today, ONDK retains 60% of their loans.

I do agree with ONDK that the short term nature of the loans makes it easier to monitor loan performance and take corrective action if necessary. Nevertheless, I do think the institutional imperative is a powerful force. There is a 25% chance that ONDK will shoot themselves in the foot.

Scenario #4 – Regulatory Crackdown

I find it very difficult to forecast government actions. Yet, it seems highly likely that as non-bank lenders become a bigger slice of the US economy, they will be subject to great regulatory scrutiny. Indeed, the Treasury Department put out a request for information to these companies not too long ago.

ONDK seems to be taking the correct steps to preempt a regulatory crackdown.

For example, they have reduced their reliance on shady brokers for leads. In 2012, 69% of originations came from funding advisors. In Q3 2015, that number dropped to just 25%. They are also moving toward lower risk customers that will produce less defaults and ugly collection scenarios.

Further, somewhat counter-intuitively, compliance expense actually benefits the scale player. Compliance expense is a fixed cost that can be spread over more loans reducing the expense per loan. Compliance expense also deters new entrants from entering the field.

Scenario #5 – The Next Credit Crisis

A fifth scenario is that the next credit crisis results in a large increase in defaults. I consider this likely.

The OnDeck Score is untested in a recession. My greatest fear is that the model is based on the recent past, an unprecedented period of benign credit markets. Models based on an anomalous period will not perform well when the cycle turns. For examples, the model used by underwriters, rating agencies and investors to estimate the probability of mortgage default was based on the history of credit default swaps, which unfortunately went back “less than a decade, a period when house prices soared.”[13] These models failed miserably when housing prices dropped in 2008.

Further, ONDK’s loans will likely be hit harder than average in a downturn, since the businesses they are lending to are small and fragile.

As the Wall Street Journal stated, “In moving away from FICO, most of these online lenders are betting that their new scoring models aimed at expanding credit will hold up in a tougher business environment.”[14] Only time will tell.

Scenario #5 – Rising Interest Rates

ONDK works on a very wide spread. The average APR was over 40% in 2015. ONDK’s borrowing costs are around 5% all-in. So if rates move up 25 basis points, it doesn’t actually change the economics of the business all that much.

Conclusion

Value investors traditionally stay away from companies like ONDK for two reasons. First, their model has not withstood the test of time. Second, valuing fast growing companies is a challenge. Many investors have gotten caught with their pants down by over-estimating growth.

Here, the first issue is very real. We have no idea how ONDK’s underwriting will hold up through all phases of the credit cycle. While the approach of management to this issue is reassuring, this issue requires more work. Regarding the second issue, in my back of the envelope valuation calculation I have assumed a dramatically slower growth rate.

Finally, I think value investors are slow to appreciate the scale advantages that tech companies enjoy, particularly data network effects.

[1] OnDeck December 1, 2015 Investor Deck.

[2] OnDeck, Response to US Treasury Department Request for Information on Online Marketplace Lending and Expanding Small Business Access to Capital, 9/30/15

[3] Federal Reserve Bank of New York (2014), available at http://www.newyorkfed.org/smallbusiness/Spring2014/pdf/full-report.pdf.

[4] http://mattturck.com/2016/01/04/the-power-of-data-network-effects/

[5] Noah Breslow, 08.10.15 , Pacific Crest Global Technology Leadership Forum

[6] Entrepreneur, “Why Small Businesses Are Turning to Online Lenders,” April 15, 2015.

[7] http://www.federalreserve.gov/newsevents/speech/brainard20150930a.htm#f11

[8] On Deck Capital Inc at Goldman Sachs Financial Technology Conference September 10, 2015

[9] See e.g. Malik, Om (December 30, 2015), “In Silicon Valley Now, It’s Almost Always Winner Takes All,” New Yorker.

[10] Buffett, Warren, 2004 Letter to Shareholders.

[11] Buffett, Warren, 1986 Letter to Shareholders.

[12] On Deck Capital Inc Earnings Conference Call , May 4, 2015

[13] Salmon, Felix (2009-02-23). “Recipe for Disaster: The Formula That Killed Wall Street”. Wired.

[14] Rudegeair, Peter (2016-01-11). “Silicon Valley: We Don’t Trust FICO Scores”. Wall Street Journal.